In early 2024, the world felt like it was spinning out of financial control. Inflation was a constant headline. Interest rates were high. Most people felt like they were just trying to keep their heads above water. I remember staring at my bank account and feeling like I was working for my debt rather than for myself. That is when I revisited the Dave Ramsey budget principles.

By March 2026, the economic landscape has shifted again. While some costs have stabilized, the “genie in a bottle” of online spending is more aggressive than ever. To win today, you cannot just “try” to save money. You need a proven framework that ignores the trends and focuses on human behavior.

This guide breaks down 12 essential Ramsey budgeting tips for the current year. We will explore the Dave Ramsey 7 baby steps explained for a modern context and how to use the EveryDollar budget to reclaim your income. If you are tired of being broke, it is time to get gazelle intense.

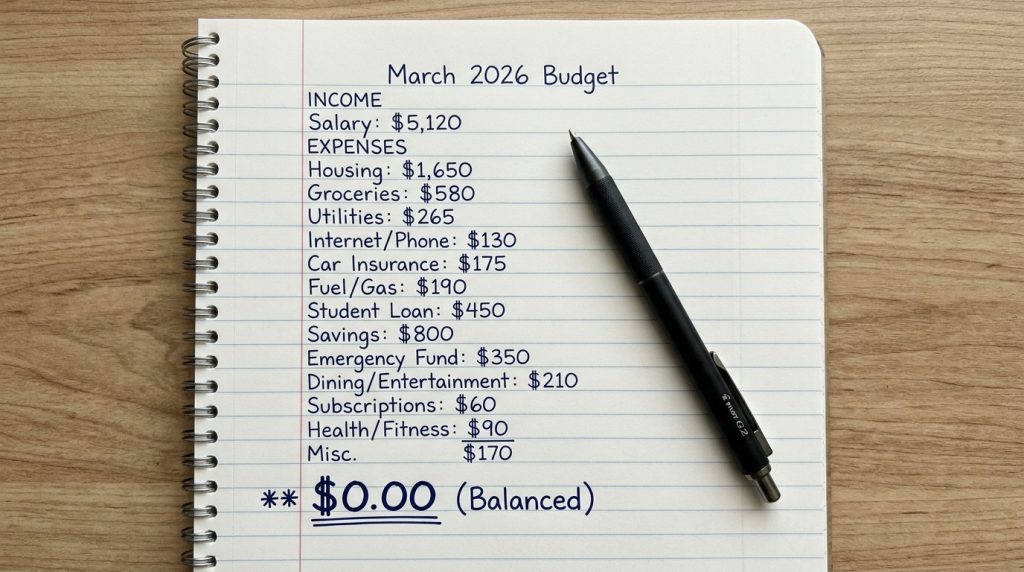

1. Master the Zero Based Budget

The foundation of the Ramsey system is the zero based budget. This means your income minus your expenses must equal exactly zero every single month. You are giving every single dollar a name before the month even begins.

In 2026, we have too many “invisible” leaks. Subscriptions, small app purchases, and digital tips add up fast. When you do a monthly budget Dave Ramsey style, you account for these first. You don’t “hope” there is money left at the end of the month. you decide where it goes on day one.

If you are new to this, Dave Ramsey budgeting for beginners starts with a simple list. Write down your take-home pay. Then, list every single expense until you hit zero. If you have $50 left over, that $50 goes toward your current Baby Step.

2. Secure Baby Step 1: The $1,000 Foundation

Baby step 1 is to save $1,000 for a starter emergency fund as fast as possible. Critics in 2026 argue that $1,000 isn’t enough due to inflation. Ramsey Solutions still holds firm on this number for one reason: it is supposed to make you nervous.

This $1,000 is a “starter” fund. It keeps a flat tire or a broken tooth from ending up on a credit card. It provides a psychological buffer while you move into the harder stages of the plan. It is your first win in the journey toward debt free living Ramsey tips.

“The goal of Baby Step 1 is not to be comfortable. The goal is to get you through the storm so you can focus 100% of your energy on killing your debt.” — Dave Ramsey

3. Launch the Debt Snowball Method

Once your $1,000 is safe, it is time for Baby Step 2. This is where you pay off all debt except the house using the debt snowball method. You list your debts from smallest balance to largest balance, regardless of interest rates.

You pay the minimum on everything except the smallest debt. You attack that smallest one with everything you have. When it is gone, you take that entire payment and “roll” it into the next debt. This creates a “snowball” effect of momentum and psychological victory.

Mathematically, some prefer the “Avalanche” (highest interest first). But Ramsey argues that personal finance is 80% behavior. You need the “win” of seeing a debt disappear to stay motivated for the long haul.

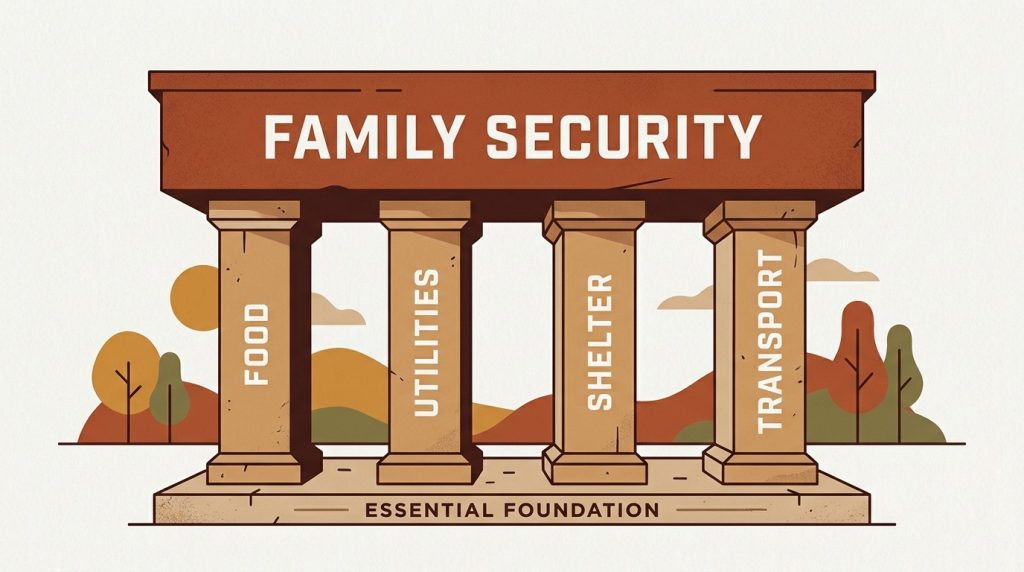

4. Prioritize the “Four Walls” First

If you find yourself in a crisis in 2026, you must protect your “Four Walls” before anything else. Even before your debt snowball. The Four Walls are:

- Food

- Utilities

- Shelter (Rent or Mortgage)

- Transportation

You pay for these before you pay the credit card company. You pay for these before you pay the student loan. If your Four Walls aren’t secure, you cannot function. This is a core part of how to do zero based budget Ramsey when times are tough.

5. Adopt the Rice and Beans Budget

To get out of debt fast, you must live like no one else. Ramsey calls this the rice and beans budget. It is a scorched-earth approach to spending. You cut out all dining out, all vacations, and all non-essential shopping.

In 2026, this means auditing your digital life. Delete the food delivery apps. Cancel the streaming services you don’t watch daily. This level of gazelle intensity is temporary. You are trading a few years of sacrifice for a lifetime of freedom.

6. Utilize EveryDollar for Digital Tracking

The every dollar budget app is designed specifically for this system. In 2026, the Premium version offers “Bank Connect,” which streams your transactions directly into your budget. This removes the “I forgot to track it” excuse.

The app also features a “Financial Roadmap” that shows your progress through the Baby Steps. It calculates your “Millionaire Date” based on your current savings rate. Seeing that date on a screen is a massive motivator to keep pushing.

| Feature | Free Version | Premium (2026) |

| Zero-Based Budgeting | Yes | Yes |

| Custom Categories | Yes | Yes |

| Automatic Bank Sync | No | Yes |

| Net Worth Tracking | No | Yes |

| Group Coaching | No | Yes |

7. Build a Fully Funded Emergency Fund

After you are debt-free (except the house), you move to Baby Step 3. This is where you grow that $1,000 into 3 to 6 months of full expenses. This is your “Big Defense” against job loss or major medical issues.

In 2026, many people aim for the 6-month mark due to the shifting job market. If you are self-employed or have a variable income, lean toward the 6-month side. This fund gives you the “power of the walk-away.” It gives you total peace.

8. Commit to 15% for Retirement

Baby Step 4 is where the wealth building truly begins. You invest 15% of your gross household income into tax-advantaged retirement accounts like a Roth IRA or 401(k).

For 2026, the IRS has raised contribution limits. You can now put up to $24,500 into your 401(k) and $7,500 into an IRA. If you are 50 or older, use the catch-up contributions to accelerate your growth.

9. Say No to Credit Cards Forever

One of the most “controversial” debt free living Ramsey tips is the total rejection of credit cards. Ramsey argues that even with “points” and “cashback,” people spend more when using plastic than when using cash.

In 2026, the “Buy Now, Pay Later” (BNPL) trap is everywhere. Ramsey calls these “scams” that keep you broke. To win with money, you must break the cycle of spending money you haven’t earned yet. If you can’t pay for it today with a debit card or cash, you can’t afford it.

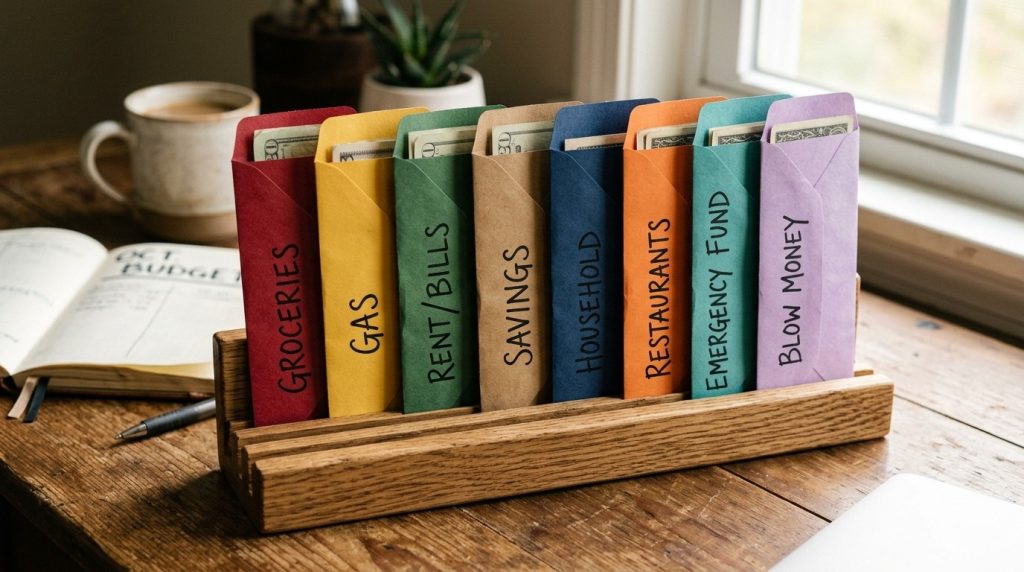

10. Use the Cash Envelope System (Digital or Physical)

For categories where you tend to overspend, like groceries or “fun money,” use cash. When the envelope is empty, you stop spending. This creates a physical “pain” of payment that digital transactions hide.

If you hate carrying physical cash, you can use the “Digital Envelope” feature in EveryDollar. You assign a specific amount to a category, and once it hits zero, you are done for the month. This discipline is what separates the wealthy from the broke.

11. Protect Your Progress with Term Life Insurance

You cannot have financial peace if your family is one tragedy away from poverty. Ramsey advises against “Whole Life” or “Universal Life” insurance, calling them “high-fee garbage.”

Instead, get a 15- or 20-year term life policy for 10 to 12 times your annual income. This is pure protection. It is cheap and effective. It ensures that if something happens to you, your baby steps budget and legacy are protected for your loved ones.

12. Live and Give Like No One Else

The final step, Baby Step 7, is the most fun. You have no debt, your house is paid off, and you are building wealth. Now, you can be “outrageously generous.”

The goal of the Dave Ramsey budget isn’t just to have a big pile of money. It is to have the freedom to help others and change your family tree. Whether it is supporting a local charity or helping a friend in need, giving is the ultimate reward of financial discipline.

Dave Ramsey 7 Baby Steps Explained (The Order)

- $1,000 Starter Emergency Fund: Your “First Defense.”

- Debt Snowball: Pay off all debt except the house.

- 3-6 Months of Expenses: Your “Full Defense.”

- 15% to Retirement: Build your future.

- College Funding: Save for your kids’ education.

- Pay Off the Home Early: Total freedom.

- Build Wealth and Give: The ultimate goal.

Frequently Asked Questions

Is $1,000 still realistic for Baby Step 1 in 2026?

Formally, yes. While the cost of living has risen, the purpose of the $1,000 fund is to keep you “uncomfortable.” If you have a large buffer, you might lose your gazelle intense focus on Step 2. However, some financial coaches suggest $2,000 if your “Four Walls” costs are extremely high.

Can I invest while I am in Baby Step 2?

Dave Ramsey recommends pausing all investing, including 401(k) matches, while in Baby Step 2. This allows you to throw 100% of your focus and margin at the debt. The goal is to get out of Step 2 in two years or less.

Does the Debt Snowball work with high interest rates?

Yes. The snowball is about behavior, not math. If you attack the high-interest debt but never see a balance disappear, you are more likely to quit. By knocking out small debts first, you gain the psychological momentum needed to finish the journey.

How do I handle a variable income with EveryDollar?

Use your “lowest expected” income for your monthly plan. If you earn more, treat it as a “windfall” and apply it immediately to your current Baby Step. This ensures you are always covered on your Four Walls.

Conclusion

Budgeting in 2026 is an act of rebellion. The world wants you to spend, stay in debt, and keep up with influencers. By following these Dave Ramsey budget tips, you are choosing a different path. You are choosing peace over payments.

Start tonight. Open a spreadsheet or download EveryDollar and name every dollar of your next paycheck. Whether you are on Baby Step 1 or paying off your mortgage, the only wrong move is standing still.