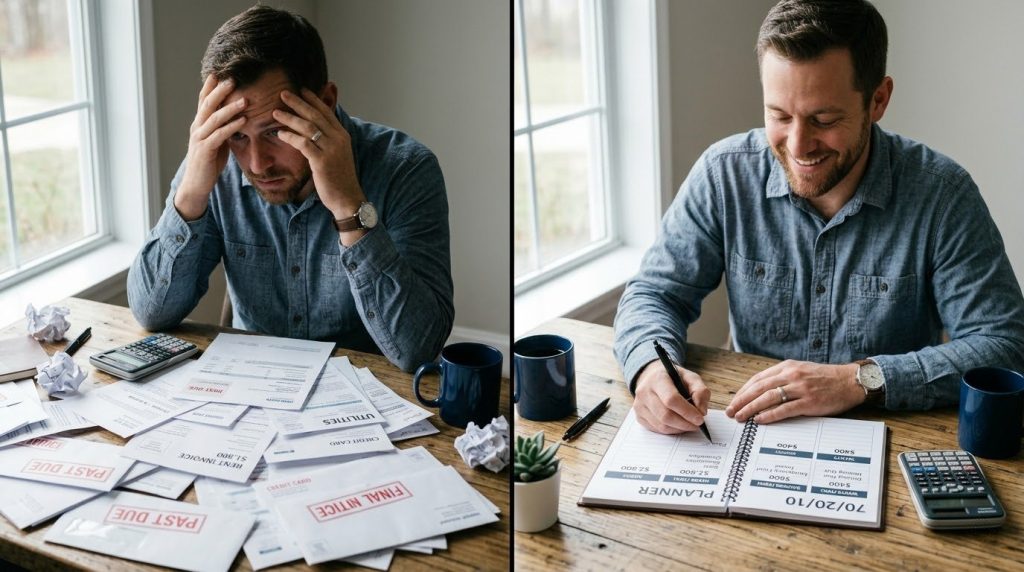

In March 2024, I stared at a spreadsheet that looked like a crime scene. I had four different savings accounts. I had three credit cards with balances that made me want to hide under my bed. I was trying to follow every piece of Money Management Advice I found online. None of it stuck. I felt like I was working for my bank rather than for my future. Everything felt too complex. I was exhausted by the math.

By early 2026, the world changed. Inflation stayed high. Rent in cities like Karachi and New York soared. The old ways of saving felt impossible. That is when I stripped everything back to the 70/20/10 Budget Rule. It is the simplest framework I have ever used. It doesn’t require a degree in finance. It doesn’t require hours of tracking every single coffee.

This guide is the result of my two year journey from chaos to clarity. I will show you exactly how the 70 20 10 Rule actually works in 2026. We will look at building a Travel Fund, utilizing High Yield Savings, and the grit required for Paying Off Credit Cards. If you want to stop feeling like a slave to your paycheck, this is your exit ramp.

1. What is the 70/20/10 Budget Rule and why does it work?

The 70 20 10 Rule is a simple way to divide your take home pay. You put 70% toward your essentials. You put 20% toward savings and debt. You put the final 10% toward your wants and fun. It is a Budgeting system designed for speed and simplicity. It removes the decision fatigue that kills most financial plans.

In 2026, we are bombarded with choices. We have too many apps. We have too many subscription services. Most Budget Rules fail because they are too restrictive. The 70/20/10 model is different. It gives you a large enough bucket for your life while ensuring your future is protected. It is the ultimate tool for Managing Your Money without the stress.

I found that this rule works because it matches the reality of a high cost of living. When rent is 40% of your income, a 50/30/20 budget feels like a lie. The 70% bucket is large enough to be honest. It allows you to breathe while you are Paying Off Credit Cards. You can see more about foundational planning in my financial freedom roadmap.

2. Breaking Down the 70% Why Essentials are the Foundation

The largest portion of your income goes to your “Four Walls.” This includes housing, transportation, food, and utilities. In 2026, these costs are higher than ever. If you spend more than 70% on these items, you are “house poor.” I learned this the hard way when I moved into a luxury apartment that took up 55% of my check.

To make the 70 20 10 Rule work, you must be ruthless with your recurring bills. I spent a Saturday afternoon calling my internet and insurance providers. I saved $120 a month just by asking for a better rate. This is the core of Money Management Advice. Every dollar you save in the 70% bucket moves to your wealth building bucket.

If your essentials are over 70%, you have an income problem or a lifestyle problem. I had to sell a car I couldn’t afford to get my numbers back in line. It was painful but necessary for Financial Freedom. For more tips on cutting costs, check out my how to save money on groceries guide.

3. The 20% Growth Pillar Building Wealth and Paying Off Debt

This is the most important bucket for your future. The 20% goes toward your Emergency Fund, retirement, and Paying Off Credit Cards. In 2025, I was only saving 5%. I felt like I was spinning my wheels. When I moved to a strict 20%, my net worth finally started to move.

I recommend putting this money into a High Yield Savings account immediately. Do not let it sit in your checking account. If you see it, you will spend it. I use Ally Bank because their buckets feature makes it easy to see my progress. This is a vital part of Managing Your Money effectively.

If you have high interest debt, this 20% should attack that first. Credit card interest is a tax on the disorganized. I used the “Debt Snowball” method to kill $15,000 in debt in eighteen months. You can learn the exact steps in my how to get out of debt post.

4. The 10% Lifestyle Rule Why Fun is Not Optional

Most people think they have to suffer to be rich. They are wrong. If you don’t have a “fun” bucket, you will eventually rebel against your own budget. The 10% is for your hobbies, dining out, and shopping. It is your guilt free spending money.

In 2026, I use this 10% for my Travel Fund. I save $300 a month for a yearly trip to the mountains. Knowing that money is set aside allows me to enjoy my life today. It prevents the burnout that comes with extreme frugality. This is a key part of Budget Rules that people often ignore.

If you want to go out for a fancy dinner, go for it. Just make sure it fits in the 10%. If the 10% is empty, you stay home. This simple boundary is one of the best Money Saving Habits I have ever developed. See my best side hustles to start now if you want to grow this fun bucket.

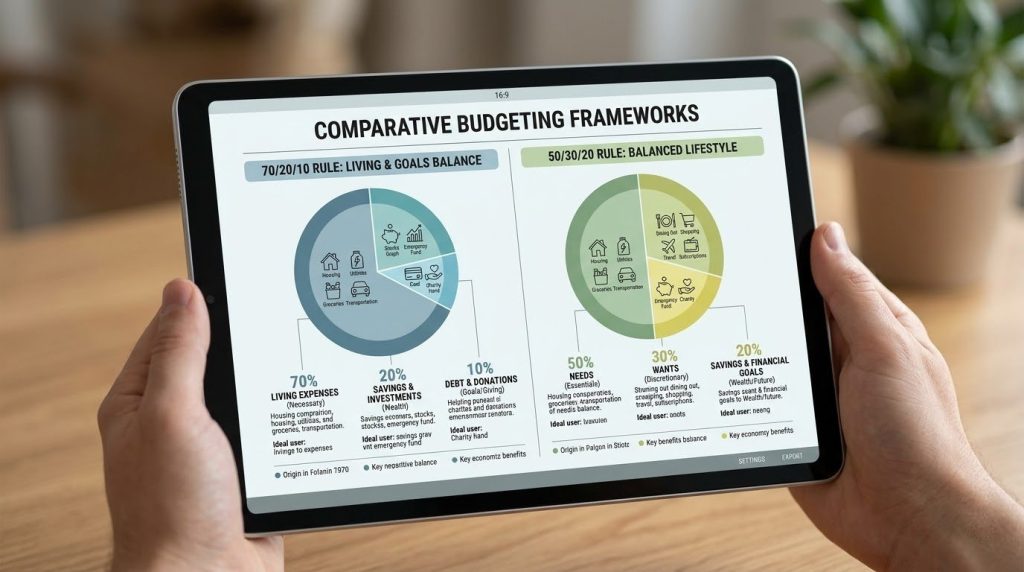

5. How the 70/20/10 Rule Compares to Other Systems

| Budget Rule | Essentials | Savings/Debt | Fun/Wants | Best For |

| 70/20/10 | 70% | 20% | 10% | High Cost Areas |

| 50/30/20 | 50% | 20% | 30% | High Earners |

| 80/20 | 80% | 20% | (Included) | Simple Tracking |

| Zero-Based | 100% | (Allocated) | (Allocated) | Perfectionists |

I found that the 70/20/10 Budget Rule is the most realistic for 2026. Most families cannot live on 50% of their income for essentials anymore. The 70% bucket acknowledges reality while the 20% bucket ensures growth. It is the middle ground we all need.

If you are a beginner, do not start with a complex system. Start with this one. It provides the most clarity with the least amount of effort. You can find a Monthly Budget Template to help you get started in my how to budget for beginners guide.

6. Case Study How Sarah Escaped the Paycheck Cycle

Sarah was a 32 year old graphic designer earning $4,500 a month. She was constantly stressed. Her rent was $1,800. Her car payment was $500. She was barely making the minimum payments on her cards. She had no Money Management Advice that actually worked for her life.

In June 2025, she adopted the 70 20 10 Rule. She realized her essentials were actually at 82%. She took a radical step and moved to a smaller apartment. She also started a small freelance hustle on the side. Within six months, her essentials were down to 68%.

She took the extra 22% and focused on Paying Off Credit Cards. By March 2026, she was debt free. She now has a $10,000 High Yield Savings account and a growing Travel Fund. Her story is proof that the system works if you are willing to make the big moves. See how to make money on pinterest for more ideas like Sarah’s.

7. Setting Up Your High Yield Savings for Success

If your savings are in a traditional bank, you are losing money. In 2026, High Yield Savings accounts are offering 4% or more. A traditional bank offers 0.01%. On a $10,000 balance, that is a difference of $400 a year. That is “free” money for your Travel Fund.

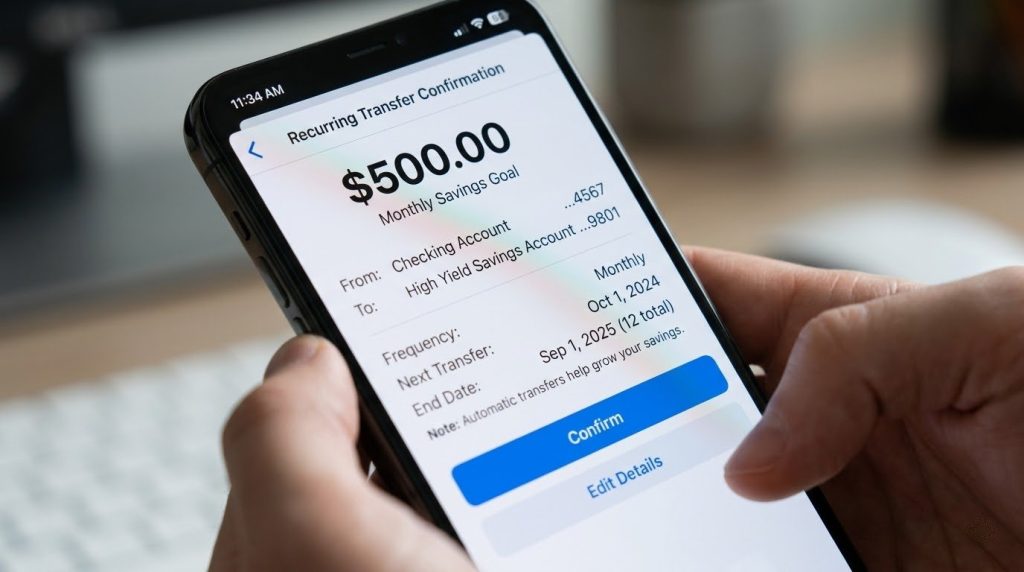

I recommend setting up three separate accounts for your 20% bucket. One for your Emergency Fund. One for your retirement. One for your debt payments. This separation prevents you from “borrowing” from your future to pay for today. It is a cornerstone of Managing Your Money.

Automation is your best friend. Set your bank to transfer the money the day you get paid. If you wait until the end of the month, the money will be gone. This is the most practical Money Saving Challenge you can give yourself. For more on asset building, see stock market investing for beginners.

8. Managing Your Money on a Variable Income

If you are a freelancer or business owner, the 70 20 10 Rule still works. You just have to base it on your lowest expected monthly income. I call this my “Floor Income.” Anything I earn above that goes straight into my High Yield Savings or my Travel Fund.

In 2024, my income swung by $2,000 month to month. I felt like I was on a roller coaster. By using the “Floor” method, I stayed stable. I never overspent in my essentials because I knew what my baseline was. This is essential Money Management Advice for the modern worker.

Keep a separate account for your taxes. Do not include your tax money in your 70% essentials. That money belongs to the government. Once the taxes are out, then apply the 70/20/10 Budget Rule. Check my emergency fund guide for more on handling income dips.

9. The 30 Day Money Saving Challenge to Kickstart Progress

If you feel overwhelmed, start with a 30 day challenge. For one month, track every single dollar that leaves your pocket. I used a physical notebook for this. It forced me to see my Bad Money Habits in black and white.

During this month, try to lower one major bill. Cancel one subscription you don’t use. Cook every meal at home for a week. These small wins build the momentum you need for a permanent 70 20 10 Rule lifestyle. It is about building the muscle of discipline.

At the end of the month, look at your percentages. If you are at 80% essentials, don’t panic. Just pick one thing to change next month. This is how you win the long game of Managing Your Money. For more inspiration, read my financial freedom roadmap.

10. How to Build a Travel Fund Without Guilt

I used to feel guilty every time I booked a flight. I felt like I was stealing from my future. When I started the 70 20 10 Rule, that guilt vanished. My 10% “Fun” bucket is specifically for these moments. I call it my “Life Bucket.”

I save for my Travel Fund in a dedicated High Yield Savings account. I call the account “Adventure.” Every time I see the balance grow, I feel a sense of accomplishment. It makes the daily grind feel worth it. This is why the 10% is so important.

If you want to travel more in 2026, you have to prioritize it. Stop spending the 10% on random Amazon purchases. Save it for the flight. This is the best way to live a rich life while Managing Your Money. See best side hustles to start now for ways to boost your travel budget.

11. Overcoming the Low Income Trap in 2026

I know what it’s like to earn a low wage. In 2023, my essentials were 95% of my income. I couldn’t “budget” my way out of that. I had to increase my “top line.” This is the reality that many Money Management Advice articles ignore.

If you are in this trap, your focus should be 100% on increasing your skills. Take a course. Start a micro-hustle. The 70 20 10 Rule is a goal to work toward, not a stick to beat yourself with. Start by saving $10 a month. Just start the habit.

Persistence is more important than the initial dollar amount. Once your income grows, keep your lifestyle the same for six months. This “Lifestyle Freeze” allows you to finally hit the 70/20/10 ratios. Check my how to budget for beginners guide for more on the low income grind.

12. Advanced Tips for Creating Wealth Fast

Once you have mastered the 70 20 10 Rule, you can get aggressive. I eventually moved to a 60/30/10 split. I kept my essentials at 60% and moved 30% into investments. This is how you reach Financial Freedom in years rather than decades.

Utilize your employer’s 401k match. That is a 100% return on your money. If you don’t take it, you are leaving money on the table. This should be part of your 20% savings bucket. It is the easiest way to start Creating Wealth in 2026.

Stay curious about new financial tools. I use Empower to track my net worth across all accounts. It gives me a high level view of my progress. This transparency is vital for long term success. Read stock market investing for beginners to see how to put your 30% to work.

13. Frequently Asked Questions

What if my rent is 50% of my income?

This is very common in 2026. If your rent is 50%, the rest of your essentials (food, gas, utilities) must stay under 20% to fit the 70 20 10 Rule. If that is impossible, you must look at increasing your income or finding a roommate. You cannot afford to skip the 20% savings bucket. That is your only way out of the cycle.

Should I pay off debt or save for an emergency fund first?

Always build a “Starter” Emergency Fund of $2,000 first. This prevents you from going deeper into debt when a tire pops or a laptop breaks. Once that is in place, use the rest of your 20% bucket for Paying Off Credit Cards. High interest debt is a financial emergency.

Is the 10% for fun too small?

It can feel small at first. But remember, the 70% includes your basic groceries and transport. The 10% is for “extra” joy. If you want more fun money, you have to find it in the 70% bucket or earn more. This discipline is what builds long term Financial Freedom.

Where is the best place for my Travel Fund?

A High Yield Savings account is the best spot. You want the money to be safe and accessible, but you also want it to earn interest. I avoid putting my Travel Fund in the stock market because I might need the cash in a few months, and I don’t want to risk a market dip.

How often should I review my 70/20/10 budget?

I do a “Money Minute” every Sunday. I check my spending for the week and see if I am on track. On the first of every month, I do a deeper dive to see if my percentages are still correct. Consistent review is the secret to successful Managing Your Money.

14. Conclusion

The 70 20 10 Rule changed my life because it gave me permission to be human. It stopped the endless cycle of guilt and math. In 2026, we need simple systems that work with our busy lives. By focusing on your essentials, your growth, and your joy, you are building a balanced life.Don’t wait for a “perfect” time to start. Take your last bank statement and run the numbers tonight. See where you are. Even if you are far from the 70/20/10 split, knowing the truth is the first step toward change. You have the power to create your own Financial Freedom.