Two years ago, I sat on my kitchen floor with three maxed out credit cards. My bank account showed exactly $14.22. I felt like a failure. I had a good job in Chicago but no clue where my money went. I tried every app. I bought every planner. Nothing stuck because I was using systems built for robots. People are not robots. We have bad days. We buy overpriced coffee when we are sad. We forget to log transactions.

You do not need more willpower. You need a system that fits your specific brain. Most financial gurus preach a one size fits all path. They are wrong. What works for a single freelancer in Austin will not work for a family of five in Seattle. This guide breaks down the best ways to manage your cash. I have tested these personally. Some saved my life. Others were total disasters.

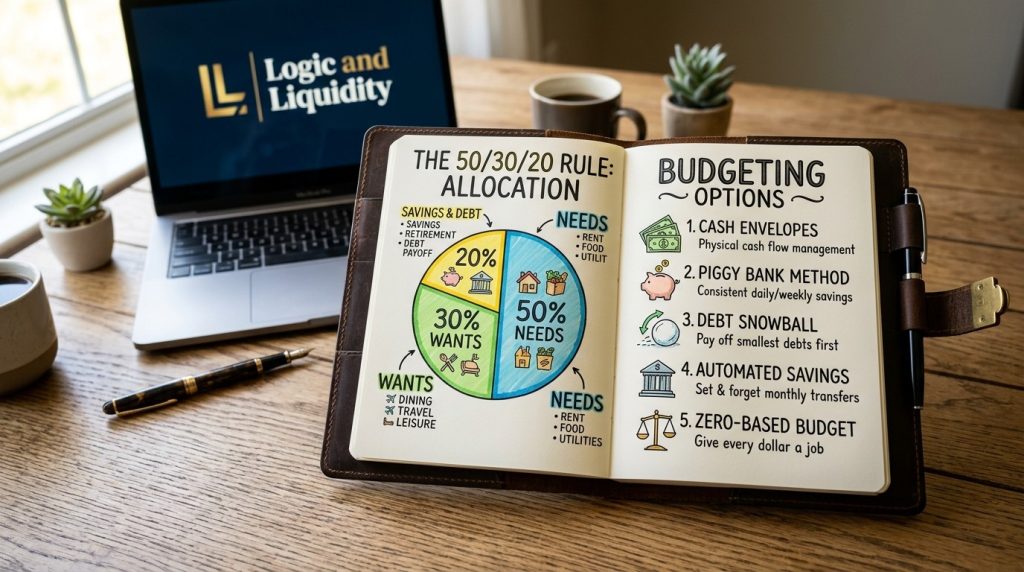

1. The 50/30/20 Rule

This is the gold standard for Budgeting For Beginners. It is simple. You split your after tax income into three piles. 50 percent goes to needs like rent and groceries. 30 percent goes to wants like dining out or Netflix. 20 percent goes to savings or debt.

My brother used this when he started his first job in 2023. He struggled to define a want versus a need. Is high speed internet a need? In 2026, yes. Is a premium gym membership a need? Probably not. You must be honest with yourself here. This 50 30 20 Budget provides a high level view without tracking every penny. It prevents burnout.

2. Zero Based Budgeting

Every single dollar gets a job. If you earn $5,000 this month, you must assign all $5,000 to a category. This includes savings. Your end balance should be zero. This is a great Budget Plan for people who wonder where their money went.

I used this method to pay off $12,000 in car debt. It forced me to face my spending habits. You cannot hide from a zero based system. I recommend using a tool like YNAB for this. It is $99 a year now. That price is steep but the software is powerful. It stops you from spending money you do not have yet.

3. The Envelope System

This is a classic for a reason. You take cold, hard cash. You put it in physical envelopes labeled for specific categories. Once the grocery envelope is empty, you stop eating. It sounds harsh. It is.

I tried this in 2022. I went to the grocery store in downtown Denver. I forgot my envelope on the counter at home. I had to leave a full cart of food at the register. I felt embarrassed. But I never forgot my cash again. Physical cash creates a psychological pain when you spend it. Swiping a card feels like nothing. Giving away a twenty dollar bill feels like a loss.

4. Pay Yourself First

Stop waiting until the end of the month to save. Most people pay their rent, their phone bill, and their bar tab first. They save whatever is left. Usually, nothing is left. This method flips the script.

Set up an automatic transfer. Move your savings goal to a high yield account the moment your paycheck hits. I suggest Ally Bank or SoFi. They offer around 4.5 percent interest right now. Treat your savings like a bill you cannot skip. If you do not see the money, you will not spend it. This is the fastest way to build an emergency fund.

5. The 60 Percent Solution

Richard Jenkins created this. It is a variation of the 50/30/20 Rule. You keep your committed expenses to 60 percent of your gross income. The remaining 40 percent is split. 10 percent goes to retirement. 10 percent goes to long term savings. 10 percent goes to short term savings. 10 percent is for fun.

This works well for high earners who hate tracking. It focuses on the big picture. If your rent is too high, this system breaks. I saw a friend try this in San Francisco. Her rent was 55 percent of her pay. She had no room for fun. You must have a low cost of living for this to thrive.

6. Values Based Budgeting

Stop spending on things you do not care about. This is not about restriction. It is about intention. You look at your spending. You ask if it brings you joy or moves you toward your goals.

I used to spend $150 a month on clothes I never wore. I shifted that money to a travel fund. Last year, I went to Japan for two weeks. I did not miss the fast fashion. I loved the sushi. This is a great Budgeting Planner strategy for emotional spenders. It turns “no” into “yes” for things that matter.

7. The Anti Budget

This is for people who hate spreadsheets. You focus on one number. How much do you need to save? You pull that out immediately. You spend the rest however you want.

It sounds risky. It can be. But if you hit your big goals first, the details matter less. I used this during a high stress season at work. I did not have the energy to log receipts. I just made sure my 401k and IRA were full. My bank balance was low at the end of the month, but my net worth grew.

8. The 70/20/10 Rule

This is a conservative approach. 70 percent goes to living expenses. 20 percent goes to debt or savings. 10 percent goes to tithing or charity.

This is a solid How To Budget model for those with strong community values. I know a couple in Nashville who use this. They live on 70 percent to ensure they can give back 10 percent to their local food shelf. It keeps them grounded. It prevents lifestyle creep. When they get a raise, they keep the ratios the same.

9. The Weekly Allowance Method

Take your monthly spending money. Divide it by four. That is your weekly limit. This prevents the “first of the month” splurge.

I struggled with spending $400 in the first week of a month. By week three, I was eating ramen. This method fixed that. I gave myself $150 every Monday morning. When Sunday rolled around, I usually had $10 left. It felt like a game. This is perfect for those who struggle with long term planning.

10. Proportional Budgeting

This is a customized version of the 50 30 20 Budget. You set your own percentages based on your life stage. Maybe you are in debt payoff mode. Your split might be 50/10/40.

A freelancer I know in New York uses this. His income fluctuates. He uses a 40/30/30 split. 40 percent for taxes and business. 30 percent for life. 30 percent for his future. It gives him a Budget Plan that breathes. He adjusts the numbers every quarter.

11. No Spend Challenge

This is a short term reset. You commit to spending zero dollars on non-essentials for a set time. A weekend, a week, or a month.

I do a no spend January every year. It clears the holiday brain fog. I only buy groceries and gas. I found that I saved an extra $800 last time. It reminded me that I have enough stuff. Use this when you feel out of control. It is a mental detox for your wallet. It provides excellent Money Saving Methods data. You see exactly where your triggers are.

12. Half Payment Method

Take your big bills. Split them in half. Pay half from your first paycheck. Pay the other half from the second.

This is a life saver for people who live paycheck to paycheck. Rent can feel like a mountain on the first of the month. My cousin in Phoenix used this. He sent $1,000 to his landlord on the 15th and the other $1,000 on the 1st. It kept his bank account balance steady. No more “big bill” anxiety. Most landlords or utility companies are fine with this if you ask.

13. 80/20 Budgeting

This is the simplest version of a plan. Save 20 percent. Spend 80 percent. That is it.

It lacks detail but it builds a habit. If you are a student or just starting out, do this. Do not worry about categories yet. Just learn to live on less than you make. I started here in college. I saved $50 from every $250 paycheck. It felt like a lot then. It set the stage for my future.

14. Calendar Budgeting

Write your expenses on a physical or digital calendar on the day they are due. Match them with your paydays.

Visual learners love this. I use Google Calendar for this. I see a “Rent” block on the 1st. I see a “Payday” block on the 15th. It shows me the gaps in my cash flow. I can see that week two is “heavy” with bills. I plan my grocery trips for week one instead. This is a very practical How To Make A Budget step.

15. Bare Bones Budgeting

This is your emergency plan. It only includes what you need to survive. Shelter, basic food, utilities, and transport. No Netflix. No eating out. No new shoes.

Everyone needs a bare bones list. I calculated mine during the 2020 lockdowns. I realized I could live on $2,200 a month if I had to. Knowing that number gave me peace. If I lost my job today, I know exactly what to cut. It is your financial fire escape.

16. Spending Fasts

Choose one category to cut out for a month. Coffee. Clothes. Uber rides.

I did a coffee fast in October. I saved $180. I realized I liked my home brew just as much. These fasts are great Money Saving Methods because they challenge your identity. I thought I was a “coffee shop person.” I was just a person who liked caffeine. You can find these Budget Examples all over social media. They provide quick wins.

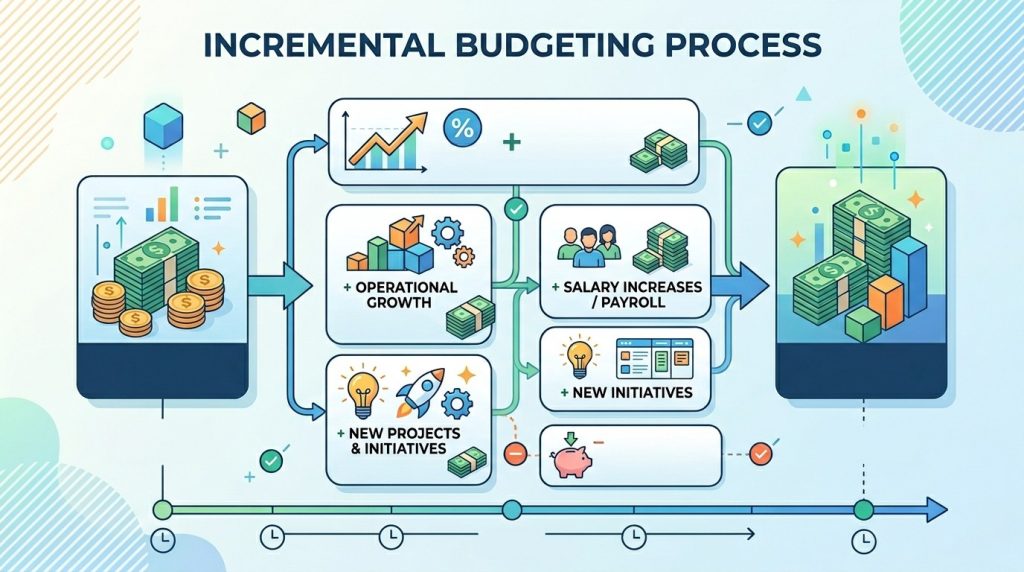

17. Incremental Budgeting

Take last month’s budget. Adjust it by a small percentage based on new goals or changes.

This is for people with stable lives. If your rent goes up $50, you trim $50 from another spot. It is about small tweaks, not huge overhauls. My parents have used this for thirty years. They know their baseline. They just adjust for inflation or a new hobby. It is low stress and highly sustainable.

18. Goal Oriented Budgeting

You don’t care about categories. You only care about the goal. You want a house. You want a wedding. You want a Tesla.

You work backward from the price tag. If a house down payment is $40,000 in two years, you need $1,666 a month. You find that money wherever you can. It makes the sacrifice feel worth it. When I was saving for my first house, I didn’t care about eating lentils. I wanted that backyard. The goal was the fuel.

19. Hybrid Budgeting

Mix and match any of these. Use the Envelope system for groceries. Use the 50/30/20 rule for the rest.

Most experts won’t tell you this. You are allowed to change the rules. I use a zero based budget for my business and an anti budget for my personal life. It works for me. If a system feels like a straitjacket, you will quit. Make it your own.

20. The “No Budget” Budget

This only works if you are naturally frugal and earn way more than you spend. You check your balance. You spend when you need to. You don’t spend when you don’t.

I do not recommend this for most people. I tried this for six months. I ended up spending $2,000 on “miscellaneous” items. It is too easy to lose track. Use this only if you have a massive cash cushion and a history of low spending. For the rest of us, we need a map.

Comparison of Popular Methods

| Method | Complexity | Best For | Main Tool |

| 50/30/20 | Low | Beginners | Simple Sheet |

| Zero Based | High | Debt Payoff | YNAB |

| Envelopes | Medium | Overspenders | Physical Cash |

| Anti-Budget | Low | Busy People | Automation |

| 60% Solution | Medium | High Earners | Spreadsheet |

How To Make A Budget That Sticks

Planning is easy. Following through is hard. I have seen hundreds of people start a Budget Plan on January 1st. By February 10th, they are back to old habits. The secret is not more data. The secret is psychology.

First, identify your “why.” If you are just doing this because a blog told you to, you will fail. You need a deep reason. Maybe you want to stop fighting with your spouse about money. Maybe you want to quit a job you hate. Write that reason on a sticky note. Put it on your laptop.

Second, forgive yourself. You will mess up. You will buy a round of drinks for your friends. You will forget a subscription renewal. Do not throw away the whole month. Just start again tomorrow. I used to let one mistake ruin my whole week. Now, I just log the expense and move on.

Third, use the right tools. I have tried 15 different apps. Some are too complex. Others are too buggy. Here are my honest thoughts on current options.

8 Tools to Help You Succeed

- YNAB (You Need A Budget). The best for changing behavior. It costs money, but it saves more than it costs.

- Empower. Great for seeing your net worth and investments. It is free but they will try to sell you wealth management services.

- Rocket Money. Excellent for finding and canceling hidden subscriptions. The interface is very user friendly.

- EveryDollar. Dave Ramsey’s tool. Good for zero based budgeting without the complexity of YNAB.

- Tiller. It feeds your bank data directly into Google Sheets. Perfect for spreadsheet nerds who want automation.

- Goodbudget. A digital version of the envelope system. Great for couples who want to share a budget.

- PocketGuard. Simple and shows you exactly how much “in my pocket” money you have left.

- Monarch Money. A newer contender that is very polished. It is a great Mint alternative.

Common Fail Points and How to Avoid Them

Why do most plans fail? I have coached dozens of friends through this. The same problems pop up every time.

The “Miscellaneous” Trap. You have a category for everything. Then you have a “misc” category that eats 20 percent of your pay. Stop doing this. If you spend money on it, name it.

Ignoring Annual Fees. Your Amazon Prime or car registration comes due. It feels like an emergency. It is not. It is a predictable expense. Divide the cost by 12. Save that much every month.

Being Too Restrictive. If you love coffee, do not cut it to zero. You will rebel. Give yourself a small “fun” budget. It is the pressure valve for your financial life.

Not Checking In. A budget is a living thing. You must look at it at least once a week. I do a “Money Monday” ritual. I spend 15 minutes reviewing my trades and spending. It keeps me sharp.

Frequently Asked Questions

Which budgeting method is best for debt?

Zero based budgeting is the most powerful for debt. It forces you to see every dollar. You can then direct every extra cent to your smallest balance. This creates momentum. My friend Sarah used this to kill $30k in student loans in two years. She lived on rice and beans, but she is free now.

How do I budget with an irregular income?

Use a hill and valley fund. During good months, save the extra in a separate account. During slow months, pull from that account to pay yourself a steady “salary.” This works for freelancers and sales people. Never budget based on your best month. Budget based on your average or lowest month.

Should I use an app or a spreadsheet?

It depends on your personality. Apps are faster. Spreadsheets are more customizable. I prefer a spreadsheet for my long term goals and an app for my daily spending. Try both for a month. See which one you actually open.

How much should I save for emergencies?

Start with $1,000. This covers most small disasters like a flat tire. Then, aim for three to six months of expenses. If your bare bones budget is $3,000, you need $9,000 to $18,000. This is your “peace of mind” fund. It is not for investing. It is for safety.

Can I budget with a partner?

Yes. Communication is critical. We use a “yours, mine, and ours” system. We have a joint account for bills. We each have a personal account for fun. We don’t judge each other’s fun spending. This prevents 90 percent of money fights.

What if I am already behind on bills?

Stop saving for a moment. Focus on the “Four Walls.” Food, utilities, shelter, and transport. Contact your creditors. Many have hardship programs. Do not hide from the phone calls. Honest talk often leads to better payment terms.

Is the 50/30/20 rule realistic in high cost cities?

It is very hard in places like New York or LA. You might need to adjust to 60/20/20. Or find ways to lower the 50 percent. This usually means a roommate or no car. If your “needs” are 70 percent, you are in the “danger zone.” You need to increase your income or move.

How often should I update my budget?

Review it weekly. Update it monthly. Life changes. Your grocery prices go up. Your gym raises its rates. A monthly check ensures your plan matches reality. I do my big update on the last Sunday of every month.

Does budgeting limit my freedom?

The opposite is true. A budget gives you permission to spend. When I have $100 in my “eating out” category, I don’t feel guilty buying a steak. I know the rent is already paid. Budgeting is the path to true freedom.

What is the biggest mistake beginners make?

They try to be perfect. They want a perfect spreadsheet on day one. Forget perfection. Focus on awareness. Just track where your money goes for 30 days. That data is more valuable than any “perfect” plan.

Can I include my 401k in my 20 percent savings?

Yes. Your 401k contributions from your paycheck count toward your savings goal. If you put 10 percent in your 401k, you only need to save another 10 percent elsewhere. This makes the goal feel much more achievable.

How do I handle sudden windfalls?

Use the 10 percent rule. Spend 10 percent on something fun. Use the other 90 percent for your current financial goal. This rewards your hard work without blowing the whole gain. I did this with a $2,000 tax refund. I bought a nice dinner and put $1,800 into my house fund.

Moving Forward With Your Money

You now have the tools. You have the Budget Examples. You know How To Budget. The only thing left is to start. Don’t wait for Monday. Don’t wait for the first of the month. Open your banking app right now. Look at your last five transactions. Was that money spent on purpose?

If not, pick one method from this list. Try it for 30 days. If you hate it, switch. Financial health is a marathon. I spent years failing before I found my rhythm. Now, I sleep through the night. I don’t fear the mailbox. You can get there too. Your future self is counting on you to make a choice today.