Introduction

Managing money in today’s fast-paced world can feel overwhelming. Bills pile up, subscriptions auto-renew, and before you know it, your paycheck has vanished without a trace. If you’ve ever reached the end of the month wondering where all your money went, you’re not alone — and you’re exactly who the zero based budget was designed for.

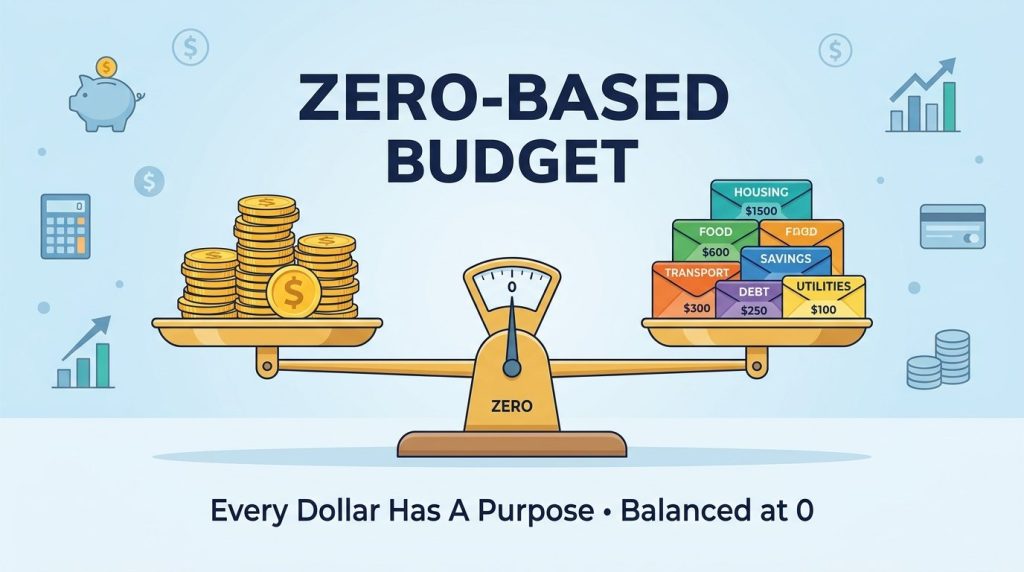

A zero based budget is one of the most powerful personal finance tools ever created. Unlike traditional budgeting methods that merely track spending after the fact, this system requires you to assign every single dollar a purpose before the month even begins. The result? Total money control, zero financial surprises, and a real path to achieving your goals — whether that’s paying off debt, building an emergency fund, or finally taking that dream vacation.

In this guide, we’re breaking down 10 simple, actionable steps to build your very own zero based budget from scratch. Whether you’re a complete beginner or someone who’s tried other budgeting systems and failed, this step-by-step approach will give you the clarity and structure you need. We’ll also cover how tools like the no spend challenge can supercharge your progress, and why having a reliable budgeting system matters more than willpower alone.

Executive Summary

A zero based budget works on one core principle: income minus expenses equals zero. That doesn’t mean you spend everything you earn — it means every dollar is allocated intentionally, including savings and investments. This blog walks you through 10 practical steps to build this budgeting system from the ground up. From listing all your income sources to daily spending tracking and monthly reviews, each step builds on the last to give you complete financial control. Key concepts covered include income listing, expense categorization, prioritizing essentials, debt repayment planning, savings allocation, and how integrating a no spend challenge can help you reset financially. By the end, you’ll have a working framework for long-term money control.

Step 1: List All Your Income Sources

The foundation of any effective zero based budget is knowing exactly how much money is coming in each month. This sounds simple, but many people underestimate or overlook certain income streams.

Start by listing every single source of income: your primary salary, freelance income, rental income, side hustle earnings, child support, government benefits, or any other regular inflows. Be conservative with variable income — if your freelance work fluctuates, use the lowest amount you’ve earned in the past three months as your baseline.

For those with irregular income, a good practice is to budget based on your minimum predictable earnings and treat any additional income as a bonus that gets allocated to debt repayment or savings. This conservative approach to money control ensures your budget doesn’t collapse in a low-income month.

Key action: Write down your total monthly take-home income (after taxes) at the top of your budget sheet. This is your starting number — every other step works from here.

Step 2: List All Your Monthly Expenses

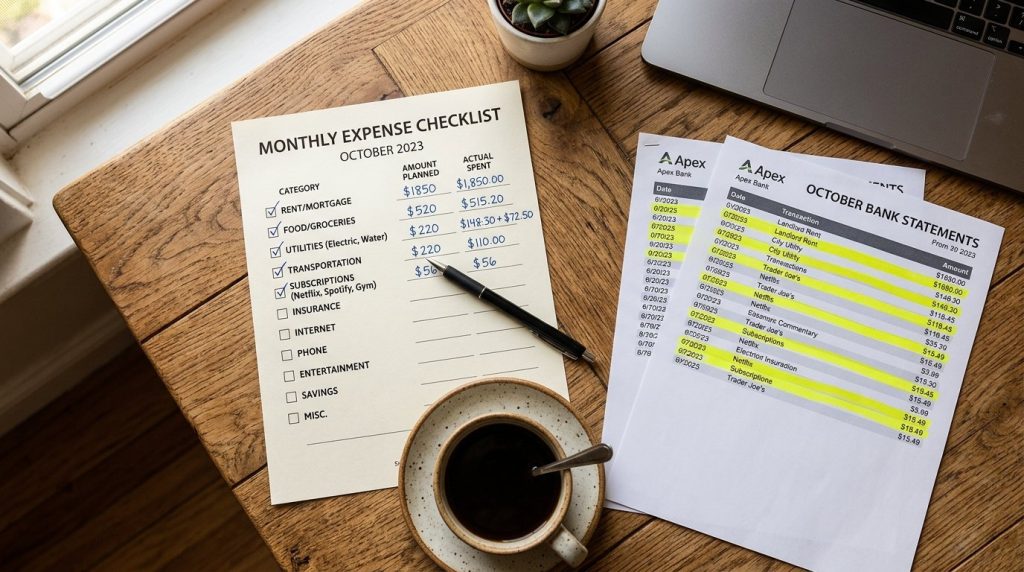

Once you know what’s coming in, it’s time to capture everything going out. This step requires honesty and thoroughness. Pull up your last three months of bank and credit card statements and categorize every single expense.

Your expense list should include fixed expenses (rent/mortgage, car payment, insurance premiums, loan repayments), variable necessities (groceries, utilities, fuel), discretionary spending (dining out, entertainment, clothing), and irregular expenses (annual subscriptions, car maintenance, medical bills). For irregular expenses, divide the annual cost by 12 and budget that amount monthly as a sinking fund.

This step is where most people get their first wake-up call. Seeing all your expenses laid out in black and white is often shocking — but it’s also the most empowering part of building a budgeting system. You can’t change what you don’t see.

Internal link: For more on how to identify and manage hidden expenses, check out our guide on building an emergency fund from scratch.

Step 3: Categorize Your Spending

Raw expense data is useful, but organized data is transformative. In this step, you’ll group all your expenses into meaningful categories that make your zero based budget easier to manage and monitor.

Common budget categories include: Housing, Transportation, Food, Utilities, Healthcare, Debt Repayment, Personal Care, Entertainment, Savings & Investments, and Giving/Charity. You can customize these to fit your lifestyle — the key is that every expense has a home.

Good categorization is what turns a list of numbers into a functional budgeting system. It shows you at a glance where your money is going and makes it obvious where adjustments are needed. For example, you might discover that “Food” is consuming 35% of your income when the recommended range is 10–15%.

Color-coding or using separate columns for “needs” vs. “wants” can make this step even more powerful, especially if you’re preparing for a no spend challenge or trying to identify areas to cut back.

Step 4: Assign Every Dollar a Job

This is the heart of the zero based budget. Once you have your total income and your complete expense list, it’s time to assign every single dollar a specific purpose until income minus all allocations equals zero.

Here’s how it works in practice: If you earn $4,000 per month, you must allocate all $4,000 across your expense categories — rent, food, savings, debt repayment, etc. — until nothing is left unassigned. If you have $200 left over after all expenses, that $200 must be assigned somewhere: extra debt payment, vacation fund, emergency savings.

This step enforces intentionality. When every dollar has a job, there’s no room for aimless spending. This is what makes the zero based budget uniquely powerful for money control — it eliminates the “I don’t know where it went” phenomenon entirely.

Pro tip: Use a budgeting app like YNAB (You Need a Budget) or EveryDollar to automate this process. Both are built specifically around zero based budgeting principles.

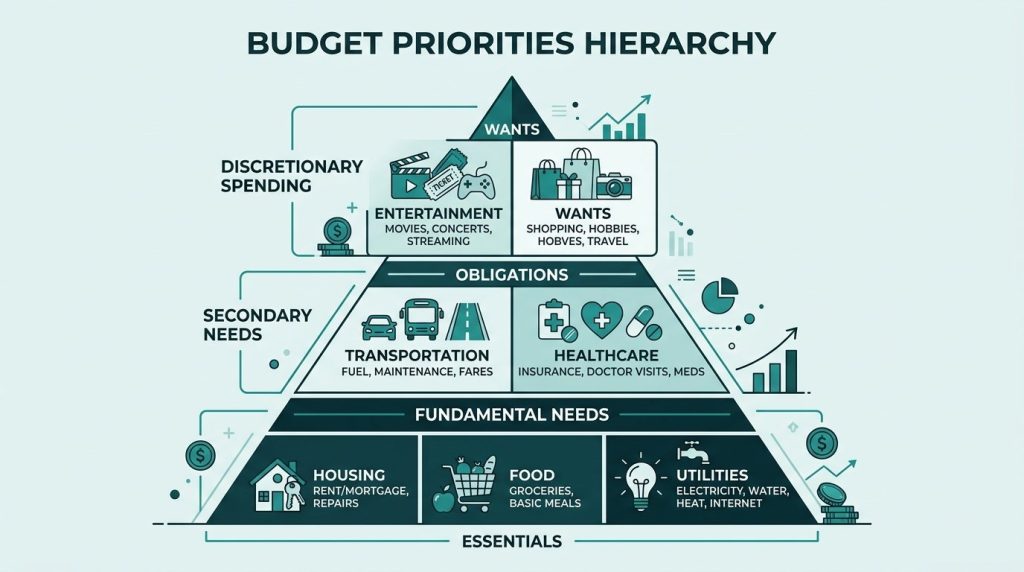

Step 5: Prioritize Essential Expenses First

When filling in your budget categories, always fund the essentials before anything else. Essential expenses are non-negotiable survival needs: housing, utilities, basic groceries, transportation to work, and minimum debt payments.

A practical hierarchy for prioritizing expenses looks like this: first, housing and utilities; second, food; third, transportation; fourth, minimum loan payments; fifth, all other necessities. Only after these are covered do you allocate money to wants, entertainment, or discretionary spending.

This priority structure protects the integrity of your budgeting system. Life happens — and when it does, you need to know that your most critical needs are already funded. It also helps you make faster, calmer decisions when unexpected expenses arise mid-month.

For families, this step often reveals trade-offs that need family discussions. Involving your household in prioritization decisions builds shared commitment to your money control goals and reduces financial conflicts.

Step 6: Allocate Money for Savings

One of the most common mistakes in personal finance is treating savings as an afterthought — something you’ll do with “whatever’s left over.” In a zero based budget, savings is a non-negotiable expense category, not a bonus.

Financial experts commonly recommend the “pay yourself first” principle: allocate savings before discretionary spending, not after. Your savings categories might include an emergency fund (target: 3–6 months of expenses), retirement contributions, a house down payment fund, a vacation sinking fund, or a car replacement fund.

Even if you can only save $50 per month right now, assign it a place in your budget. Small, consistent contributions compound significantly over time. If you’re just starting your budgeting system, prioritize building a starter emergency fund of $1,000 before aggressively tackling other financial goals.

Internal link: Learn more about how to build your emergency fund faster in our article on smart savings strategies for beginners.

Step 7: Plan for Debt Repayment

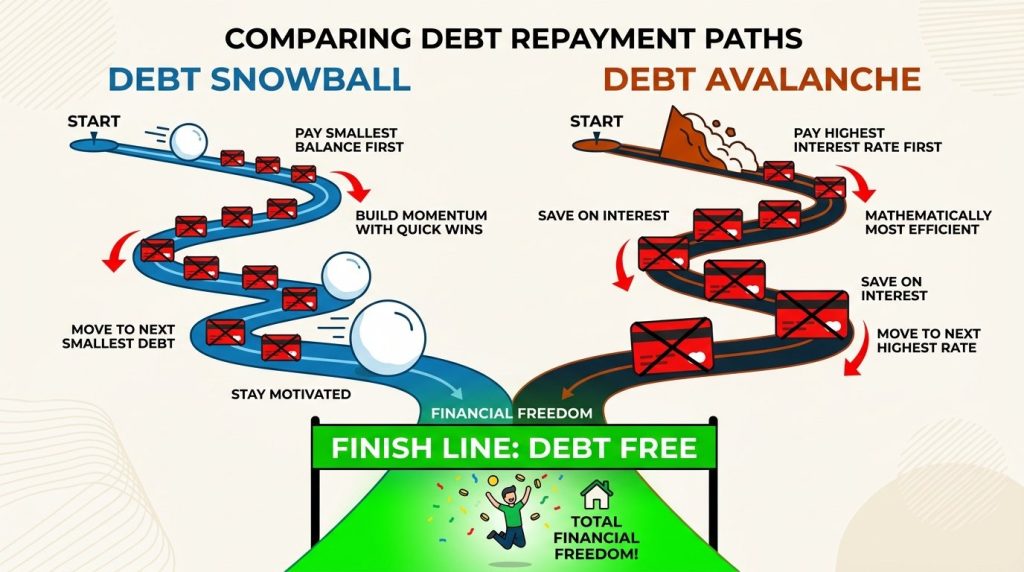

Debt is one of the biggest obstacles to financial freedom, and a zero based budget is one of the most effective tools for eliminating it. By giving debt repayment its own dedicated budget line, you make consistent progress rather than paying the minimum and hoping for the best.

Two popular debt repayment strategies work well within a zero based budgeting framework. The debt snowball method has you pay minimums on all debts while throwing extra money at the smallest balance first — the quick wins build momentum. The debt avalanche method targets the highest-interest debt first, which saves the most money mathematically.

Whichever method you choose, the key is consistency. Every month, the debt repayment line item in your budget gets funded before discretionary spending. This transforms debt elimination from a vague aspiration into a concrete, scheduled activity.

If you’re overwhelmed by debt, consider complementing your budget with a no spend challenge — a set period where you cut all non-essential spending and redirect those funds toward debt. Even a 30-day no spend challenge can make a significant dent in your balances.

Step 8: Budget for Fun and Wants

A sustainable zero based budget isn’t a punishment — it’s a plan. Completely eliminating all discretionary spending is a recipe for budget burnout and eventual abandonment. Step 8 is about allocating money for things you enjoy, guilt-free.

After covering essentials, savings, and debt repayment, assign a reasonable amount to entertainment, dining out, hobbies, clothing, and other lifestyle expenses. The difference between a healthy budget and a deprivation budget is intentionality: you’re choosing how much fun money to allocate, rather than letting it drain away unnoticed.

This step is also where a no spend challenge can be introduced strategically. Rather than eliminating fun permanently, you designate specific months or weeks as no-spend periods to reset spending habits, save more aggressively, or recover from an unexpected expense. It’s a temporary tool for extraordinary money control — not a permanent lifestyle.

Being realistic here matters. If you allocate zero dollars for entertainment but you know you’ll spend at restaurants weekly, your budget will fail by week two. Build a realistic plan you can actually live with.

Step 9: Track Your Spending Daily

Creating a zero based budget is only half the work. The other half is following it — and that requires daily tracking. Tracking your spending in real time is what separates people who succeed with this budgeting system from those who quit after a month.

Daily tracking doesn’t have to be complicated. It can be as simple as logging each transaction in a spreadsheet, using a budgeting app, or even keeping receipts and updating your budget every evening. The goal is to always know where you stand relative to your monthly allocations.

When you see that you’ve spent $180 of your $200 grocery budget by the 20th of the month, you can adjust your behavior with 10 days still to go. Without tracking, you’d only discover the overspend when reviewing your bank statement — after the damage is done.

Daily tracking also builds a powerful habit of financial mindfulness. Over time, you’ll start naturally making more conscious spending decisions because money control becomes part of your daily routine rather than an occasional exercise.

Step 10: Review and Adjust Your Budget Monthly

No zero based budget is perfect from day one — and that’s completely fine. The tenth and final step is committing to a monthly budget review where you assess what worked, what didn’t, and what needs to change for next month.

Your monthly review should cover: comparing actual spending vs. budgeted amounts in each category, identifying consistent overspending areas, adjusting category amounts based on upcoming known expenses, celebrating wins (debt paid off, savings milestones reached), and resetting all categories for the new month.

Life changes — income fluctuates, expenses shift, priorities evolve. Your budgeting system should reflect your real life, not an idealized version of it. The monthly review is also a great time to introduce new strategies, such as a no spend challenge for the next month, or to restructure savings goals as you hit milestones.

Consistency in review is what separates short-term budget experiments from long-term financial transformation. People who build wealth don’t just make one good financial decision — they build systems that guide hundreds of good decisions every month.

Internal link: Explore our monthly budget review template to make this step faster and more effective.

Frequently Asked Questions

What exactly is a zero based budget?

A zero based budget is a budgeting method where your total income minus your total allocated expenses equals zero. This doesn’t mean you spend all your money — savings and investments count as expense categories. The principle is that every dollar has a specific, intentional purpose before the month begins, ensuring complete money control.

How is a zero based budget different from other budgeting systems?

Unlike percentage-based budgeting (like the 50/30/20 rule) or envelope budgeting, a zero based budget requires you to start from scratch every single month. Each dollar is assigned based on current needs and goals rather than habit. This makes it more flexible and responsive to real life while still maintaining structure.

Is a zero based budget good for people with irregular income?

Yes, but with adjustments. If your income varies, base your monthly budget on your lowest expected income. In higher-income months, create a hierarchy for allocating the surplus — typically debt repayment and savings get priority. This approach makes a zero based budget work effectively even with freelance or commission-based income.

How does a no spend challenge fit into a zero based budget?

A no spend challenge is a period — typically 7, 14, or 30 days — where you commit to spending nothing on non-essentials. When integrated with a zero based budget, it acts as a financial reset tool, allowing you to redirect discretionary spending toward savings or debt repayment for a concentrated period.

What tools or apps can help me maintain a zero based budget?

Popular tools designed for zero based budgeting include YNAB (You Need a Budget), EveryDollar (created by Dave Ramsey), and Goodbudget. Spreadsheet templates in Google Sheets or Excel also work well, especially for those who prefer a hands-on approach to their budgeting system.

How long does it take for a zero based budget to show results?

Most people see meaningful results within 2–3 months. The first month is typically a learning curve where you discover your actual spending patterns. By month three, with consistent tracking and adjustment, most people report significantly improved money control, reduced financial stress, and measurable progress toward their financial goals.

Conclusion

The zero based budget is more than a financial tool — it’s a mindset shift. When you commit to giving every dollar a job, you stop being a passive observer of your finances and become an active architect of your financial future. The 10 steps outlined in this guide — from listing income and expenses, to categorizing spending, prioritizing essentials, allocating for savings and debt, budgeting for fun, tracking daily, and reviewing monthly — create a complete, sustainable budgeting system that grows with you.

Whether your goal is to escape debt, build wealth, achieve money control, or simply stop wondering where your paycheck disappeared to, the zero based budget gives you the framework to make it happen. Combine it with periodic no spend challenges, consistent daily tracking, and monthly reviews, and you’ll have one of the most powerful personal finance systems available — completely free and fully customizable.

The best time to start your zero based budget was last month. The second-best time is today. Pick up a spreadsheet, open a budgeting app, and give every dollar a job. Your future self will thank you.